We hope that you enjoyed the holidays and that 2020 is off to a great start! For us, the new year brings a new tax season and a new tax newsletter.

Our annual tax newsletter is full of tax law changes and we hope you find it helpful. Please feel free to contact your H&S tax professional if you have any questions – we are here to help!

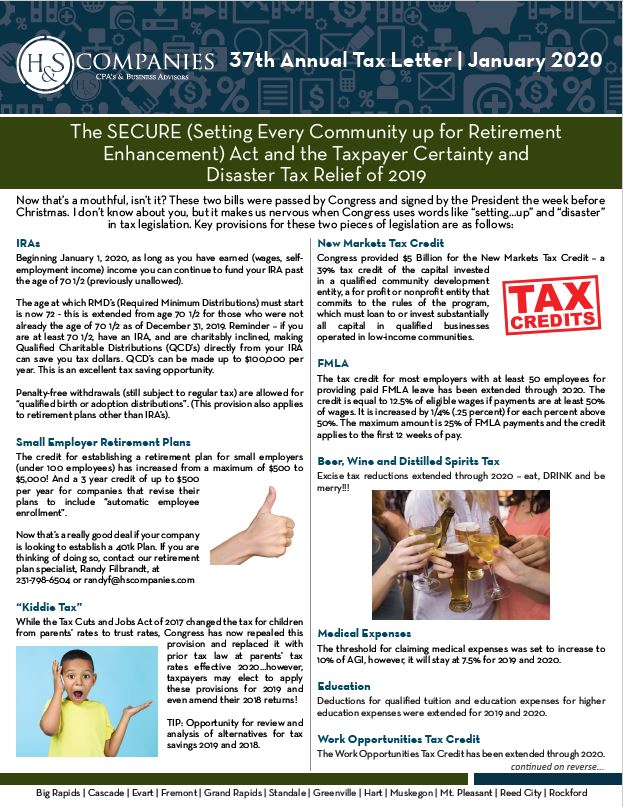

Click the image below to download a copy of our 37th annual tax newsletter. Please feel free to pass it on!

Click to Download Newsletter

If you’d also like a copy of the checklist or questionnaire, please click the links below to download:

MiBiz explains how small businesses may benefit from Pass-Through Deduction, Flat C Corp Tax Rate, Bonus Depreciation, and Accrual or Cash Accounting. The article even features our very own Sally Steffes, CPA! Click the link below to read more!

Small Business Owners See Benefits From Pass-Through Deduction, Flat Tax Rate

We hope that you enjoyed the holidays and that 2019 is off to a great start! For us, the new year brings a new tax season and a new tax newsletter.

Our annual tax newsletter is full of many new tax law changes, and we hope you find it helpful. Please feel free to contact your H&S tax professional if you have any questions – we are here to help!

Click the image below to download a copy of our 36th annual tax newsletter. Please feel free to pass it on!

Click to Download Newsletter

If you’d also like a copy of the checklist or questionnaire, please click the links below to download:

Well folks it’s here, another new year! Happy 2018! We hope you enjoyed the holidays, and were able to spend time with family and friends.

Our annual tax newsletter is full of many new tax law changes, and we hope you find it helpful. There are sure to be questions, so please feel free to contact your H&S tax professional – we are here to help!

Click the image below to download a copy of our 35th annual tax newsletter. Please feel free to pass it on!

Click to Download Newsletter

If you’d also like a copy of the checklist or questionnaire, please click the links below to download:

The election will have a large impact on tax legislation.

As the presidential race heads into the fall both candidates are campaigning hard. Many analysts have said this election will come down to the economy. With that in mind, let’s review each candidate’s position on matters that affect small business.

Code Sec. 179

Currently covers qualifying new property placed in service before January 1, 2013. Dollar limit: $139,000; Investment limit: $560,000

President Obama: Has not addressed

Mitt Romney: Has not addressed

Bonus Depreciation

Currently allows for 100% depreciation for qualified investments made after September 8, 2010 and before January 1, 2012

President Obama: Has proposed extending 100% bonus depreciation

Mitt Romney: Has discussed extending bonus depreciation, but has not indicated a percentage

Research Tax Credit

Currently allows those who participate in research to calculate this credit using the alternative simplified credit method

President Obama: Proposed to make this credit permanent and to increase the alternative simplified credit to 17%

Mitt Romney: Proposed to make this credit permanent

Code Sec. 199 Deduction

Currently allows a qualified taxpayer to deduct an amount equal or less than the phased-in percentage of taxable income or qualified production activities income

President Obama: Proposed to exclude oil, gas, coal and other producers of hard mineral fossil fuels from this credit

Mitt Romney: Has not addressed

Carried Interest

Currently allows general partners in private equity and hedge funds to charge limited partners a percentage of the fund’s earnings, aka, carried interest, which is characterized as a capital gain

President Obama: Proposed to tax as ordinary income with special rules for partners

Mitt Romney: Has not addressed

They’ve also both taken stances on things like individual rates, deductions and credits, estate tax, and the corporate tax (which we reviewed here).

Tax planning early will be difficult this year, as the presidential election will have a significant impact on tax law. Be sure to check out our October newsletter for even more tax planning ideas that may impact your tax situation for 2012.

Source: CCH Tax Briefing

The election will have a large impact on tax legislation.

Source: CCH Tax Briefing