Social Security benefits are based on an average of earnings contributed throughout a wage earner’s lifetime; so carefully reviewing your gross wage information is important. (Photo Credit: Fotolia.com)

The Social Security Administration (SSA) announced earnings and benefits statements are now available online at socialsecurity.gov.

“Our new online Social Security Statement is simple, easy-to-use and provides people with estimates they can use to plan for their retirement,” Commissioner Astrue said in a press release on the SSA’s website. “The online Statement also provides estimates for disability and survivors benefits, making the Statement an important financial planning tool. People should get in the habit of checking their online Statement each year, around their birthday, for example.”

The SSA advised people to check their Statements to ensure their earnings look correct. Social Security benefits are based on an average of earnings contributed throughout a wage earner’s lifetime; so confirming that your gross wages are accurate is important.

In February 2012, the SSA also announced they would resume mailing paper Statements to workers over age 60. They plan to begin mailing these to workers age 25 and older later this year.

To view the new tool, visit: socialsecurity.gov/mystatement

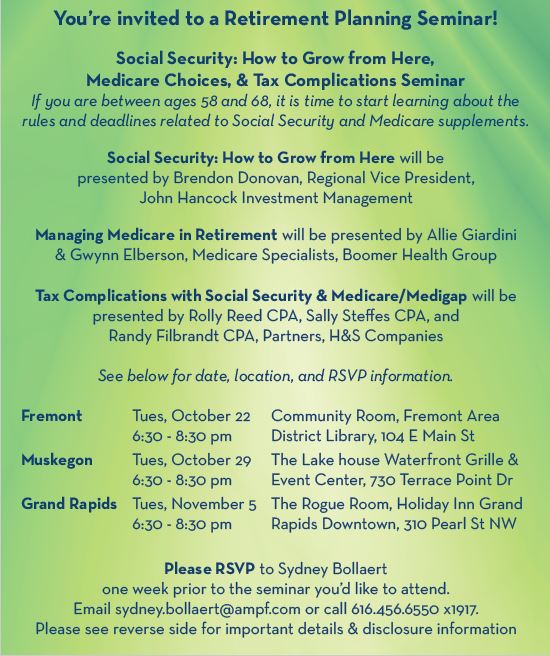

If you are between ages 58 and 68, it is time to start learning about the rules and deadlines related to Social Security and Medicare supplements. Please join us for a free seminar discussing Social Security: How to Grow from Here, Medicare Choices, & Tax Complications. We welcome you, your friends & your family members who might benefit from this information. Click on the flyer for details, locations, times and RSVP information.

If you are between ages 58 and 68, it is time to start learning about the rules and deadlines related to Social Security and Medicare supplements. Please join us for a free seminar discussing Social Security: How to Grow from Here, Medicare Choices, & Tax Complications. We welcome you, your friends & your family members who might benefit from this information. Click on the flyer for details, locations, times and RSVP information.